The Microfinance Warning Signal

On paper, India’s financial system looks clean. Bank GNPA is at a 12-year low and NBFC balance sheets are still growing. But when you zoom into microfinance, the picture changes quickly.

This is where the warning signal gets louder.

Microfinance is showing, in real time, what happens when growth starts running faster than risk control, borrower visibility and collections discipline. That is why this is not only a microfinance story. It is also a practical lesson in credit risk management, loan recovery management and better NBFC collections strategies.

The numbers make the stress hard to ignore:

- Portfolio at Risk (PAR) 31 – 180 days in microfinance almost doubled in a year, rising from about 3.8 percent to 6.8 percent of the total ₹4.14 lakh crore microfinance exposure by September 2024.

- In rupee terms, delinquencies in the 31 – 180 DPD bucket jumped from around ₹14,600 crore to over ₹28,000 crore in just 12 months.

- A Sa-Dhan report shows 30+ DPD in microfinance rising from 2.1 percent to 6.2 percent in one year, while 90+ DPD moved from 1.6 percent to 4.8 percent by March 2025.

For a collections manager, the message is simple. What may have looked like a manageable overdue bucket has become a real stress pool in barely three to four quarters.

That is why microfinance NPA trends matter beyond the sector itself. They show how fast a healthy-looking portfolio can begin to weaken when early stress is ignored, follow-up is inconsistent and borrower strain is underestimated.

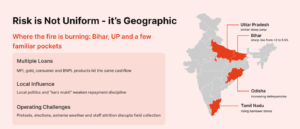

Where the fire is burning: Bihar, UP and a few familiar pockets

The stress is not evenly spread. A small group of states is carrying a large share of the damage.

Bihar, Uttar Pradesh, Tamil Nadu and Odisha together account for about 62 percent of the incremental delinquency in microfinance PAR 31 – 180 days. CRIF and Sa-Dhan data also show PAR 31 – 180 in Bihar and UP moving up sharply. In Bihar, for example, PAR 31 – 180 rose from below 2 percent to around 5.5 percent in a year, with similar jumps in UP.

What does that mean on the ground?

It means collections stress is being driven by a combination of borrower pressure and operating noise:

- Many borrowers are already carrying multiple loans across MFI, gold, consumer and BNPL products.

- All of those repayments are hitting the same household cash flow.

- Local politics and “karz mukti” messaging can weaken repayment discipline quickly.

- Protests, elections, extreme weather and staff attrition make field contact harder and less timely.

When those factors combine, the shift is fast. A borrower who is already stretched becomes hesitant. An EMI slips. Follow-up weakens. Local noise builds. Then 30+ DPD starts rising much faster than expected.

And once a microfinance borrower crosses 30 days overdue, the account can roll to 60 and 90+ very quickly if the lender does not have a tight and structured follow-up system.

That is the bigger lesson here: geography is not just branch data. It behaves like a live risk factor.

The Real Impact: Higher Credit Cost, Lower Growth

Once stress enters the portfolio, it does not stay limited to one bucket. It starts flowing through the rest of the business.

Rating agencies are already spelling that out clearly:

- ICRA expects NBFC-MFI credit cost to rise to about 320 – 340 bps in FY25, up from 220 bps the previous year, driven by higher delinquencies and provisioning.

- AUM growth for NBFC-MFIs is projected to slow from around 29 percent in FY24 to 17 – 19 percent in FY25 as lenders pull back because of asset quality concerns.

- Another ICRA note highlights that credit costs on an average managed assets basis jumped to nearly 6.8 percent in FY25 from 2.2 percent in FY24, while provision cover moved from roughly 2.8 percent of on-book portfolio to about 4.8 percent.

The chain reaction is clear:

Rising 30+ DPD → higher PAR and NPA pressure → higher provisions and write-offs → higher credit cost → lower profit → slower growth

This is why collections cannot be treated as an end-stage activity. It sits in the middle of the entire profitability equation.

For any NBFC, this is where an enterprise risk management strategy needs to stop being theoretical. The lesson from microfinance is not that overdue rises. The lesson is that overdue rises early, then moves through the book, then starts changing growth decisions, profitability and management confidence.

Why waiting for 90+ DPD is where things go wrong

One of the clearest lessons from microfinance is this: by the time an account reaches 90+ DPD, the lender is already late.

Stress does not begin there. It begins much earlier.

This is what usually happens when the system is weak:

- Early warning is poor, so nobody is watching PAR 1+ and PAR 30 closely by region, borrower type or product.

- Collections effort becomes serious only at 60+ or 90+ DPD.

- Communication is irregular, with reminders, calls, Excel sheets and WhatsApp threads all running without one consistent process.

Now look back at the numbers. PAR 31 – 180 days in microfinance doubled from ₹14,600 crore to over ₹28,000 crore in a year. That kind of movement does not appear suddenly at 90+ DPD. It starts in the earlier stages:

First, EMIs start coming in a few days late, but there is no structured pre-due reminder system. Then a borrower misses one cycle, but there is no consistent DPD1, DPD7 or DPD15 ladder. Follow-up depends on who picks the account and how disciplined that agent happens to be.

At the same time, over-leverage and local noise make the borrower pause. And because nobody reaches them with a clear, humane and practical repayment path, they stop engaging.

By the time the account crosses 90+ DPD, the situation looks very different:

- The borrower relationship is already damaged.

- Non-payment has started feeling normal.

- Recovery becomes more expensive.

- Field visits and legal action replace what could have been a simple reminder or an early intervention.

That is why 90+ DPD is not the place to start. It is the place where the cost of delay becomes visible.

The real battle is fought at 0 – 30 days.

Lessons for every NBFC, not just microfinance lenders

You may not be in microfinance. Your book may be personal loans, gold loans, two-wheeler finance or small business lending. The product may differ, but the pattern stays familiar.

1. Track stress where it starts

Do not wait for GNPA to tell you something is wrong.

Watch:

- PAR 1+

- PAR 30

- PAR 60

Track them by state, branch, product, ticket size and borrower segment. Pay closer attention to areas where AUM has grown quickly, because that is often where stress becomes visible later.

A portfolio rarely goes from healthy to broken overnight. The earlier sign is usually small: one state doubles in 30+ DPD over a few quarters or one product segment starts slipping faster than the rest.

That is where better risk scoring and early threat detection in collections become valuable. Not because they sound sophisticated, but because they help teams spot a weak signal before it becomes a portfolio-wide problem.

2. Assume borrower leverage is higher than your own system shows

Microfinance data shows a meaningful share of borrowers also carry active retail loans and borrowers with overlapping exposure show much higher 30+ DPD than those with only microfinance exposure.

For an NBFC, that means one thing very clearly: a customer who looks standard inside your CBS may still be juggling repayments from several other lenders.

Then all it takes is one event to disrupt repayment discipline:

- a job loss

- a crop failure

- a medical expense

The borrower goes from current to 30+ DPD much faster than expected.

You cannot fully control how many other loans a borrower has taken. But you can reduce the damage by acting early:

- communicate clearly before due date

- follow up quickly after the first miss

- offer simple, policy-based options when the borrower first slips

- keep the repayment path visible and easy to understand

3. Pre-due reminders are not optional

Microfinance data shows delinquencies rising even as overall exposure shrank slightly in late 2024. Lenders pulled back, but stress on existing borrowers kept building.

That tells you something important. Once repayment behavior starts weakening, late intervention becomes much more expensive than early nudging.

A simple collections hygiene ladder for any NBFC should include:

- T-7, T-3, T-1: friendly reminders over WhatsApp or SMS with the exact EMI amount and a direct payment link

- DPD 1 – 7: gentle but firm follow-up to understand whether the delay is forgetfulness or a real cash-flow issue

- DPD 8 – 30: structured communication, part-payment options where policy allows, small date adjustments within policy and escalation only when the borrower stops engaging

This is basic discipline, but it changes outcomes. It makes recovery more predictable and prevents avoidable slippages from moving deeper into the bucket.

4. Treat geography like a live risk factor

ICRA and CRIF both highlight that specific regions are driving a major share of the deterioration. That should matter to every NBFC.

Do not treat state and district data as background information. Use it actively.

That means:

- setting alert flags for districts where 30+ DPD is rising faster than the rest of the portfolio

- tightening monitoring where repayment behavior is weakening

- avoiding blind repetition of last year’s growth push in regions where DPD trends have changed

Disbursement numbers can look strong while collections quality quietly weakens underneath. The microfinance experience makes that very clear.

5. Standardize collections before stress forces you to

A common reason stress spikes so fast is that early collections remain manual and inconsistent.

That usually looks like this:

- different agents saying different things

- borrowers at the same DPD being treated differently

- half the history sitting in Excel and the rest buried in personal WhatsApp chats

When collections work like that, scaling becomes dangerous. You are no longer running a process. You are depending on effort, memory and personal style.

That is where stronger NBFC collections strategies begin: not with louder recovery action, but with better standardization.

Every lender should have a clear ladder for:

- Pre-due reminders

- DPD actions at 1, 7, 15, 30, 60 and 90 days

- Settlement and restructuring rules

- Scripts and templates that are humane and compliant

Without that, even a good portfolio can deteriorate faster than expected.

How DebtPulse helps prevent a microfinance-style collections shock

DebtPulse is built to address exactly the kind of slow-building stress that microfinance is showing now.

1. It helps you catch stress early, not at 90+

Automated pre-due reminders begin 7 days, 3 days and 1 day before EMI due date across WhatsApp, SMS and email.

Each message includes:

- the exact EMI amount

- a payment link

- a fast, simple action path for the borrower

That directly reduces the “I forgot” and “I’ll do it later” cases that later start appearing inside the 1 – 30 DPD bucket.

2. It helps teams focus on the right accounts

DebtPulse scores every account and highlights patterns by:

- state

- branch

- ticket size

- vintage

So if one pocket starts behaving like the stressed microfinance states, the signal becomes visible in the dashboard instead of staying buried inside Excel.

Your telecalling team gets a more useful priority view: the accounts most likely to cure with timely outreach rise to the top. That supports better risk scoring, sharper follow-up and stronger loan recovery management without wasting effort on accounts that do not need immediate attention.

3. It creates a standardized DPD ladder without extra IT dependence

Flows can be configured clearly:

- DPD 1: gentle SMS and WhatsApp

- DPD 7: call plus follow-up message with repayment options

- DPD 15: supervisor review and possible settlement path

- DPD 30+: structured escalation for the right profiles

This runs automatically for every account, every day. No one has to remember who is at what stage. No one has to rebuild the process manually.

That kind of consistency is exactly what many stressed collections setups are missing.

4. It gives management a live view of portfolio stress

DebtPulse tracks PAR buckets across:

- 1 – 30

- 31 – 60

- 61 – 90

- 90+

And it does that by product and geography on a live dashboard.

That means management can actually see whether 30+ DPD in a region is starting to slope upward quarter after quarter. Instead of discovering sector-style stress late, they can adjust collections, pricing and growth decisions while the problem is still manageable.

The bigger lesson from microfinance

Microfinance is today’s cautionary tale, but the lesson is broader.

Stress rarely arrives with a dramatic announcement. It builds quietly in small overdue buckets, uneven geographies, borrower overlap, delayed calls, inconsistent follow-up and operational looseness that nobody feels urgently enough to fix.

Then one quarter later, it is visible in PAR. Another quarter later, it is visible in NPA pressure. And soon after that, it shows up in credit cost, provisioning and growth slowdown.

That is why this is not only a story about microfinance. It is a story about discipline.

The clearest takeaway for every NBFC is this: do not wait for 90+ DPD to tell you there is a problem. Put pre-due nudges, early-stage follow-up, better credit risk management and structured collections workflows in place now. That is how you protect portfolio quality before stress becomes expensive.

And if your current system still depends too heavily on Excel, memory and inconsistent outreach, this is the right moment to fix it. Book a call to see how DebtPulse can help you build a more proactive collections process before a small overdue bucket turns into a much larger problem.