The 9:30 AM shock

Every morning, the first question a collection head at an NBFC asks is simple: “Kitna aaya kal?” How much came in yesterday?

That question sounds routine. It is not. It is the fastest way to tell whether the machine is still working.

From the outside, the NBFC story looks strong. Balance sheets are expanding, assets are rising and the sector appears healthy. But inside many MIS dashboards, another story is building quietly. The 90+ DPD bucket is swelling. And once money gets trapped there, it stops behaving like working capital. It becomes stuck capital. It cannot be re-lent with confidence, it starts demanding provisions and it slowly begins to choke tomorrow’s growth.

That is the real problem with NPA. It is not only about bad loans sitting on paper. It is about what those bad loans do to your future loan book. Every rupee that slips too far into delinquency is not just hurting collections today. It is reducing lending headroom for the months ahead.

This is where the pressure becomes very real. A small movement in GNPA, say from 2.7 percent to 3.5 percent, does not look dramatic at first glance. But on a meaningful book, that shift can drain profit, tighten capital and test boardroom patience much faster than many teams expect.

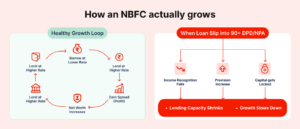

How an NBFC actually grows

Strip away the jargon and the business model is simple.

An NBFC borrows money at one rate and lends it at a higher rate. The spread between the two, after operating costs and provisions, becomes profit. That profit strengthens net worth. A stronger net worth allows the NBFC to raise more debt and grow its loan book.

When customers pay on time, the cycle is healthy. Each EMI that comes in helps the company:

- service its own lenders

- cover operating and collection costs

- support fresh disbursements

That is what smooth growth looks like.

But once loans begin slipping into NPA territory, especially 90+ DPD, the engine starts losing fuel.

Three things happen almost at once:

- income recognition gets affected

- provisions begin to rise

- capital and lending headroom get squeezed

This is why credit risk management cannot be treated as a reporting function alone. It sits at the center of growth. The issue is not simply that standard loans are good and NPAs are bad. The deeper issue is that NPAs consume the very capital required to write tomorrow’s loans.

So when leaders talk about growth, they should also be talking about loan portfolio risk. Because if the right accounts are not protected early, growth numbers can look strong on the surface while the balance sheet weakens underneath.

What 90+ DPD really means

Once an account crosses the overdue threshold and becomes an NPA, it is no longer a regular earning asset. Over time, it gets classified into buckets like sub-standard, doubtful and loss. And as that happens, the provisioning burden rises.

In plain terms, a standard loan is like stock you can still sell.

A 90+ DPD loan is like damaged stock sitting in the godown. It is still there. It still counts in outstanding numbers. But it is no longer contributing the way live stock should. Worse, you now have to write down part of its value.

That means every rupee crossing 90 DPD is a rupee you:

- cannot treat like normal earning income

- must provide against

- cannot confidently recycle into a fresh loan without more capital support

Yes, recoveries may still happen later. But from a growth standpoint, that money is on life support for a long stretch.

This is where many NBFCs underestimate the real cost of delay. By the time an account reaches 90+ DPD, the damage is not just operational. It is financial. It starts affecting profit quality, capital efficiency and future disbursement confidence all at once.

The sector may look healthy, but stress pockets are real

At the headline level, the sector picture appears stable. Growth is visible and overall GNPA levels seem manageable. But sector averages can be misleading comfort.

Stress rarely arrives with a loud announcement. It builds inside specific pockets, specific geographies, specific borrower segments and specific institutions. Some NBFCs can absorb that stress. Others cannot.

That is why the difference between sector-wide comfort and institution-level pain matters so much. A lender sitting slightly worse than the average is not just “a little behind.” That lender may already be dealing with:

- tougher questions from banks and investors

- rising cost of funds

- higher provisioning pressure

- weaker profit retention

This is exactly where NBFC risk management becomes less about broad strategy and more about daily discipline. If collections are weak, if exposures are concentrated or if accounts are allowed to drift too far before intervention, GNPA can rise faster than management teams are prepared for.

And once that happens, it is no longer just an operations issue. It becomes a board issue.

Why 2.7 percent vs 3.5 percent hurts so much

Take a simple example.

Assume your loan book is ₹500 crore.

At 2.7 percent GNPA, your NPA book is ₹13.5 crore.

At 3.5 percent GNPA, your NPA book is ₹17.5 crore.

That difference is ₹4 crore.

Now look at it from the provisioning angle. If, over time, the average provision against this 90+ DPD bucket works out to 50 percent, the picture gets sharper.

At 2.7 percent GNPA, provisions are about ₹6.75 crore.

At 3.5 percent GNPA, provisions are about ₹8.75 crore.

That is ₹2 crore of additional provisions.

And that ₹2 crore does not come from nowhere. It comes out of profit.

If the NBFC was targeting ₹20 crore profit for the year, that one movement in GNPA means a 10 percent hit to net profit. That means lower internal accruals, weaker growth in net worth and less room to leverage the balance sheet for future borrowing.

This is why a small shift in NPA ratios should never be dismissed as a rounding error. It directly affects:

- profit today

- capital tomorrow

- growth options after that

This is also why credit loss prevention has to start well before an account looks severe. Once the loan has already aged deep into delinquency, the cost of saving it becomes much higher.

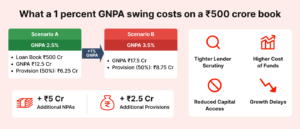

What a 1 percent GNPA swing costs on a ₹500 crore book

Now make the math even simpler.

Scenario A: GNPA at 2.5 percent

- Book size: ₹500 crore

- GNPA amount: ₹12.5 crore

- At 50 percent provisioning over time: ₹6.25 crore

Scenario B: GNPA at 3.5 percent

- GNPA amount: ₹17.5 crore

- At 50 percent provisioning over time: ₹8.75 crore

Difference

- Additional NPAs: ₹5 crore

- Additional provisions: ₹2.5 crore

That is what a 1 percent worsening in GNPA can do on a ₹500 crore book.

For a small or mid-size NBFC, ₹2.5 crore is not a cosmetic number. It can be the difference between a decent year and a difficult year. Between comfortable lender conversations and uncomfortable ones. Between growth plans moving forward and growth plans being delayed.

And remember, this is only the direct provisioning hit. The second-order effects are often just as painful:

- lender scrutiny gets tighter

- capital becomes harder to access

- the cost of funds can rise

- growth capital becomes more expensive

So no, one percentage point is not “just 1 percent.” In practical terms, it is a measure of how much of your tomorrow is already being consumed today.

Why smaller NBFCs feel this pain faster

Large NBFCs often have more room to absorb pressure. They tend to have diversified books, stronger systems and thicker capital buffers.

Small and mid-size NBFCs usually do not enjoy that kind of flexibility.

They often operate with:

- concentrated exposure by geography or borrower segment

- dependence on a limited set of bank lines or investors

- tighter capital cushions

- leaner collections teams

That means even a modest spike in NPA can trigger outsized damage.

A few accounts drifting too far can force slower disbursements. A small stress pocket can impact lender confidence. Weak collections in one cluster can spill into bigger balance sheet consequences.

This is where bad loan management stops being a backend issue and becomes a growth issue. Smaller lenders do not always lose because they took reckless bets. Sometimes they lose because good loans were allowed to become bad loans too slowly, too quietly and too manually.

The real culprit is often the collections process

In many smaller NBFCs, the collections setup still looks familiar:

- overdue accounts managed in Excel

- telecallers dialing manually

- reminders sent one by one from phones

- action starting only after EMI bounce

That setup creates predictable leakage.

High-risk accounts are followed up late. High-probability cures are not prioritised. Teams spend too much time on the wrong borrowers. There is no clear structure for reminders, negotiation, settlement or escalation.

The result is not surprising. Too many accounts move from 1 – 30 DPD to 30 – 60 and then to 90+ DPD. By then, the borrower is harder to engage, the options are fewer and the cost of recovery is much higher.

That is why the better question is not: Why are NPAs rising?

The better question is: Why are we letting good loans turn bad?

Because most borrowers do not set out to default. Slippage often begins with missed communication, temporary cash flow stress or avoidance after the first missed payment. If those moments are handled early, a meaningful portion of future NPA never reaches the NPA bucket at all.

That is the cleanest form of credit loss prevention.

How DebtPulse helps protect tomorrow’s loan book

DebtPulse is built for NBFCs that are still operating in that Excel-plus-WhatsApp world. The goal is simple: stop avoidable slippages early, structure collections better and make the cost of delay visible.

1. Stop slippages before they start

Automated reminders can go out before EMI due dates across WhatsApp, SMS and email. Borrowers receive personalised messages and direct payment links, making it easier to clear dues before the account starts aging.

The benefit is straightforward: fewer accounts enter early DPD buckets and fewer of those eventually become NPA.

2. Help agents focus on the right accounts

Instead of spreading effort evenly across all overdue borrowers, DebtPulse prioritises overdue accounts by recovery likelihood and repayment behaviour. That gives telecallers a smarter queue and clearer action path.

This improves cure rates in early buckets and supports stronger loan portfolio risk control.

3. Create a borrower-friendly collections journey

Borrowers can pay through links shared over WhatsApp or SMS, including partial payment or policy-based settlement journeys where applicable. That reduces friction and removes some of the emotional resistance that often builds after missed dues.

A smoother experience can improve self-cure rates before accounts become expensive to manage.

4. Show management what NPA is doing to growth

Collections are tagged by channel, agent and DPD bucket, making it easier to see what is working and what is not. That means management can finally connect recovery effort to provisioning savings and GNPA improvement in a visible way.

When the board asks why performance is improving, the answer becomes measurable.

5. Build auditability into the process

All borrower communication sits in one timeline. That creates structure, visibility and accountability across channels.

And in a broader operating environment where process control, conduct discipline and even conversations around cybersecurity for business are becoming harder to ignore, structured systems matter more than ad hoc workflows.

Don’t let today’s NPA eat tomorrow’s growth

The NBFC opportunity is still strong. Demand is there. Growth is there. But the strength of that story depends on one hard truth: growth only stays healthy when NPA stays controlled.

Every rupee in 90+ DPD is more than a bad number in an MIS report. It is a rupee that cannot be re-lent with confidence. A rupee that demands provisioning. A rupee that weakens profit, net worth and future lending capacity.

That is why this is not only a collection problem. It is a balance sheet problem. A growth problem. A credit risk management problem.

DebtPulse helps attack that problem at the point where it still feels manageable: before good loans become bad loans, before early stress becomes serious delinquency and before GNPA moves from tolerable to painful.

If you want to see what a 1 percent swing in NPA is really costing on your own ₹500 crore book and how structured, automated collections can protect growth before the damage compounds, now is the right time to look closely. Book a call and let the numbers speak for themselves.