Cloud based debt collection software helps lenders, NBFCs, fintech companies, and loan servicing teams manage overdue accounts, automate borrower follow ups, track repayment behaviour, and improve recovery visibility without depending on scattered spreadsheets or manual calling lists. In addition, incorporating AI fraud detection software can further enhance security and reduce risk for financial service providers.

For lenders, the problem is not just delayed EMIs. The bigger challenge is managing growing borrower volume, fragmented communication, high risk accounts, manual recovery tasks, compliance records, and portfolio performance from different systems. As lending portfolios grow, collection teams need a faster and more organized way to recover dues.

That is why modern lenders use cloud based debt collection software to centralize recovery operations, automate reminders, prioritize risky borrowers, track agent actions, and keep collection records ready for audits.

What Problem Does Cloud Based Debt Collection Software Solve?

Lenders face one major problem: they need to recover overdue payments on time without increasing team workload, losing borrower context, or creating compliance gaps.

When recovery operations are manual, small delays quickly become bigger problems. A borrower may miss an EMI reminder. A promise to pay may not be followed up. A high risk account may stay in a low priority queue. A field agent update may remain in a separate file. A borrower may receive repeated calls from different agents without proper context.

Without a proper system, collection teams usually depend on:

- Manual calling lists

- Spreadsheets

- Disconnected CRM tools

- Delayed EMI reminders

- Scattered WhatsApp, SMS, email, and call records

- Manual allocation of accounts

- Limited visibility into borrower risk

- Incomplete recovery history

These methods may work for a small loan book. But once a lender starts handling thousands of borrowers, multiple delinquency stages, and different recovery teams, manual collection becomes slow, expensive, and difficult to control.

Cloud based debt collection software solves this by giving lenders one system to track overdue accounts, automate reminders, assign tasks, monitor borrower behaviour, and improve recovery visibility.

What Is Cloud Based Debt Collection Software?

Cloud based debt collection software is an online platform that helps lenders manage overdue accounts, borrower communication, recovery workflows, repayment promises, agent tasks, and portfolio performance from a centralized system.

In fintech lending, NBFCs, and loan servicing operations, it is commonly used for:

- EMI reminder automation

- Delinquency tracking

- Borrower risk scoring

- Collection workflow automation

- Promise to pay tracking

- Multi-channel borrower communication

- Recovery agent task allocation

- Field collection updates

- Portfolio dashboards

- Compliance recordkeeping

- Audit trail creation

- Recovery reporting

In simple terms, it helps recovery teams answer important questions like:

- Which borrowers need follow-up today?

- Which accounts are becoming high-risk?

- Has the borrower received an EMI reminder?

- Did the borrower promise to pay?

- Which agent owns the account?

- What communication has already happened?

- Which accounts are moving into serious delinquency?

- Can we prove our recovery process during an audit?

For lenders, cloud based debt collection software is not just a communication tool. It is a recovery control system that helps teams act earlier and work with better visibility.

Why Do Lenders Need Cloud Based Debt Collection Software?

Lenders need cloud based debt collection software because loan recovery has become more complex, more data heavy, and more time-sensitive.

Digital lenders may disburse loans quickly, but repayment behaviour can change after disbursal. Some borrowers may miss one EMI and recover after a reminder. Some may need a repayment plan. Some may repeatedly delay payments. Others may show early signs of default before the account becomes seriously overdue.

When these signals are tracked manually, teams often react late.

A high-risk borrower may not be contacted on time. A promise to pay may be missed. Multiple agents may work on the same account without proper notes. A borrower may receive inconsistent communication. Recovery leaders may not know which portfolio segment is getting worse until the numbers show up later.

A collection management system software approach helps lenders organize these workflows in one place. It improves account tracking, borrower visibility, task allocation, and reporting, so collection teams can move from reactive follow ups to more planned recovery operations.

How Big Is the Debt Recovery Problem?

Debt recovery is becoming more important because digital lending and unsecured credit have expanded quickly.

According to CRIF High Mark, its Fintech Barometer with the Digital Lenders Association of India reported a 44% increase in delinquencies among personal loan borrowers who took loans between December 2023 and June 2024. This shows why lenders need stronger early risk detection and recovery workflows, especially in digital lending portfolios.

A Government of India parliamentary response citing RBI data showed that the GNPA ratio for unsecured retail loans increased from 1.56% in March 2024 to 1.82% in March 2025. For lenders, even a small increase in delinquency can create serious recovery pressure when loan volumes are high. Government of India parliamentary response

The RBI’s digital lending FAQs also mention that recovery or servicing of delinquent digital loans may be undertaken by recovery agents. This makes proper borrower communication records, controlled recovery workflows, and audit visibility important for digital lenders.

The broader lending environment also shows why early recovery visibility matters. Reuters, citing RBI’s Financial Stability Report, reported that retail loan delinquencies had increased in segments such as credit cards and microfinance due to stress among riskier borrowers.

These numbers show why lenders need better recovery systems. As loan volumes, borrower segments, delinquency pressure, and compliance expectations increase, manual collection operations become harder to manage.

What Are the Benefits of Cloud Based Debt Collection Software?

The biggest benefit of cloud based debt collection software is that it gives lenders one place to manage borrower follow-ups, overdue accounts, agent actions, and portfolio performance.

Instead of searching across spreadsheets, call notes, CRM entries, and message logs, recovery teams can work from a centralized system.

The main benefits include:

- Faster borrower follow ups

- Better prioritization of overdue accounts

- Lower manual workload

- Improved portfolio visibility

- More consistent borrower communication

- Better promise to pay tracking

- Stronger recovery team coordination

- Easier audit preparation

- Real time recovery dashboards

- Better control over compliance records

For NBFCs, fintech lenders, and loan servicing teams, this matters because recovery performance depends on timing, consistency, and visibility.

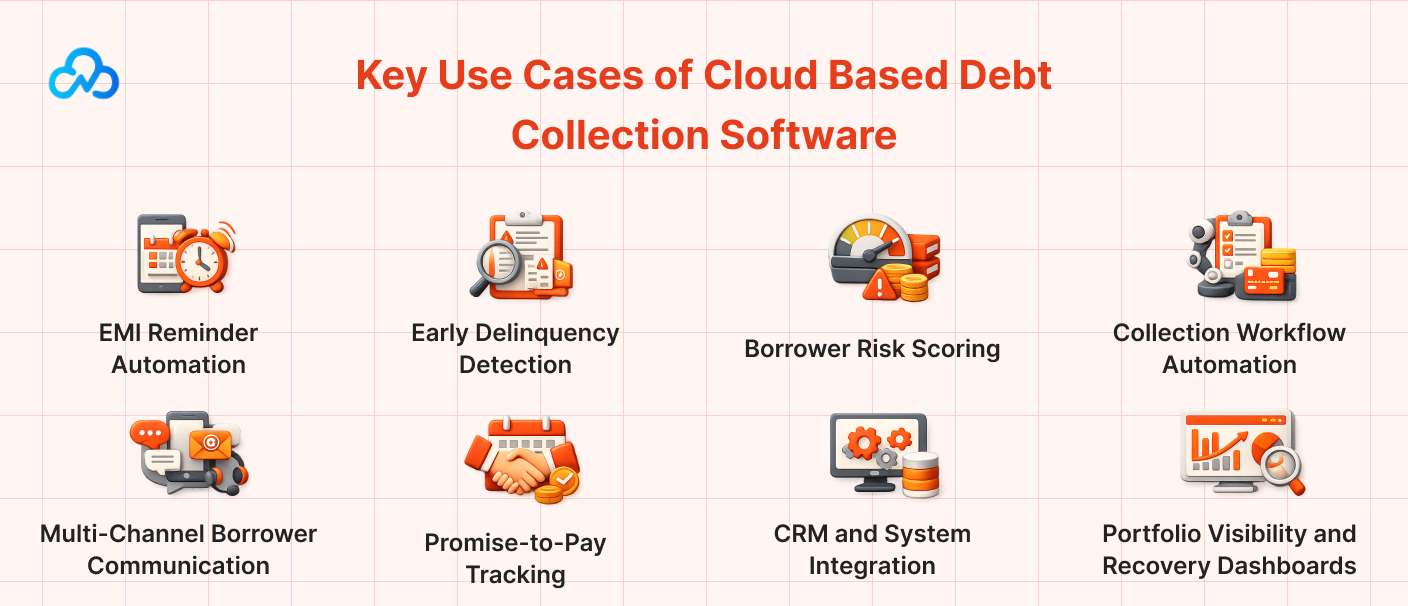

Key Use Cases of Cloud Based Debt Collection Software

1. EMI Reminder Automation

Many repayment delays happen because reminders are late, missed, or not personalized.

Debt collection automation software helps lenders send EMI reminders through channels such as SMS, WhatsApp, email, calls, or app notifications. These reminders can be scheduled based on due dates, borrower risk level, repayment history, and collection stage.

This reduces repetitive manual work and gives borrowers timely communication before the account becomes overdue.

For lenders, automated reminders can help reduce avoidable delays and free collection teams from repetitive follow-up tasks.

2. Early Delinquency Detection

Early delinquency detection helps lenders identify borrowers who may become high-risk before the account moves into serious default.

A borrower may show early warning signals through missed EMIs, failed auto-debits, repeated partial payments, delayed responses, broken promises, or sudden changes in repayment behaviour.

Cloud based debt collection software helps teams track these signals earlier and move accounts into the right collection workflow.

This is useful for:

- NBFCs

- Digital lenders

- Banks

- Loan servicing companies

- Consumer lending platforms

- Embedded finance companies

The goal is simple: contact the right borrower at the right time before the account becomes harder to recover.

3. Borrower Risk Scoring

Not every overdue account needs the same level of attention.

Some borrowers may only need a reminder. Some may need a repayment plan. Some may require faster escalation. Others may show signs of serious default risk.

A debt collection system software setup helps lenders score borrowers based on:

- Repayment history

- Missed EMI patterns

- Account age

- Delinquency stage

- Communication response

- Promise-to-pay history

- Partial payment behaviour

- Borrower segment

- Past recovery outcomes

- Portfolio risk category

This helps collection teams prioritize high-risk borrowers instead of treating every overdue account the same way.

4. Collection Workflow Automation

Collection teams often lose time because tasks are assigned manually and updates are spread across different tools.

Cloud based debt collection software helps automate workflows such as:

- Assigning overdue accounts to agents

- Triggering reminders

- Escalating high-risk accounts

- Tracking promise-to-pay dates

- Scheduling follow-up actions

- Updating borrower status

- Routing cases based on delinquency stage

- Generating collection reports

This creates a more organized recovery process and reduces dependency on manual tracking.

For large lending portfolios, workflow automation helps teams move faster without losing control over account-level actions.

5. Multi-Channel Borrower Communication

Borrowers do not respond through one channel only. Some respond to calls, some to WhatsApp, some to SMS, and some through app notifications or self-service repayment options.

Cloud based debt collection software helps lenders manage borrower communication across multiple channels while keeping records in one place.

This is important because recovery teams need to know:

- When the borrower was contacted

- Which channel was used

- What response was received

- Whether a promise-to-pay was made

- Whether the borrower needs escalation

- Whether communication followed internal policy

Centralized communication improves coordination and reduces repeated or inconsistent follow-ups.

6. Promise-to-Pay Tracking

Many borrowers do not refuse to pay. They may need more time, a smaller repayment window, or a structured repayment plan.

Cloud based debt collection software helps lenders track promise-to-pay commitments clearly.

This is useful when teams need to manage:

- Promise-to-pay dates

- Partial payments

- Broken commitments

- Rescheduled payment plans

- Settlement workflows

- Hardship cases

- Escalation approvals

A structured promise-to-pay process helps lenders improve recovery while keeping borrower communication more controlled and transparent.

7. CRM and System Integration

A common question lenders ask is whether cloud based debt collection software can integrate with CRM systems, loan management systems, payment systems, and internal tools.

This matters because collection teams need borrower data, repayment history, account status, communication notes, and payment updates in one workflow.

Good integration helps teams avoid duplicate data entry and reduces the risk of missing borrower updates.

For lenders, integration can improve:

- Borrower data visibility

- Agent productivity

- Payment update tracking

- Collection task accuracy

- Reporting quality

- Audit readiness

This is especially useful for lenders already using CRM, loan origination systems, loan management platforms, payment gateways, or customer support tools.

8. Portfolio Visibility and Recovery Dashboards

Collection leaders need visibility into portfolio performance, not just individual accounts.

Cloud based debt collection software can provide dashboards for:

- Total overdue amount

- Active delinquent accounts

- Recovery rate

- Pending promise-to-pay cases

- Roll-forward and roll-back trends

- Agent performance

- Campaign performance

- High-risk borrower segments

- Broken payment commitments

This helps collection heads and risk leaders understand where recovery is improving and where intervention is needed.

9. Compliance and Audit Tracking

Debt collection is not only about recovery. It also needs proper communication discipline, documentation, and audit visibility.

If borrower communication is not recorded properly, lenders may struggle during internal reviews, regulatory checks, or customer disputes.

Cloud based debt collection software helps maintain records of:

- Contact attempts

- Communication history

- Agent actions

- Borrower responses

- Repayment commitments

- Escalations

- Account status changes

- Recovery decisions

This makes the collection process easier to review and helps teams prove that recovery actions were handled properly.

Common Debt Collection Challenges for Lenders

Manual Follow-Ups Are Too Slow

Manual follow-ups create delays and increase workload for recovery teams. As borrower volume grows, it becomes difficult to contact every overdue account on time.

Collection Data Is Scattered

Borrower details, repayment history, communication notes, agent updates, and escalation records often sit in different systems. This makes it difficult to get a complete view of recovery status.

High-Risk Borrowers Are Not Prioritized Early

When accounts are handled in a fixed order, teams may miss borrowers who need urgent attention. This can allow early delinquency to become serious default.

Borrower Communication Becomes Inconsistent

Different agents may contact borrowers with different messages or without full context. This can hurt borrower experience and create compliance risk.

Operational Costs Keep Rising

Manual collections require more agents, more coordination, and more supervision. Without automation, recovery costs increase as portfolios grow.

Compliance Records Are Incomplete

If calls, messages, promises, escalations, and decisions are not tracked properly, audit readiness becomes difficult.

What Features Should Cloud Based Debt Collection Software Have?

A strong cloud based debt collection software platform should include:

- EMI reminder automation

- Borrower risk scoring

- Multi-channel communication

- Collection workflow automation

- Promise to pay tracking

- Agent task allocation

- Repayment plan management

- Portfolio dashboards

- Recovery performance reports

- Delinquency tracking

- Escalation workflows

- CRM or loan system integration

- Compliance recordkeeping

- Audit trails

- API integration

- Role based access

- Secure data handling

For NBFCs and fintech lenders, the most important features are automated reminders, borrower risk scoring, workflow automation, portfolio visibility, compliance tracking, and recovery reporting.

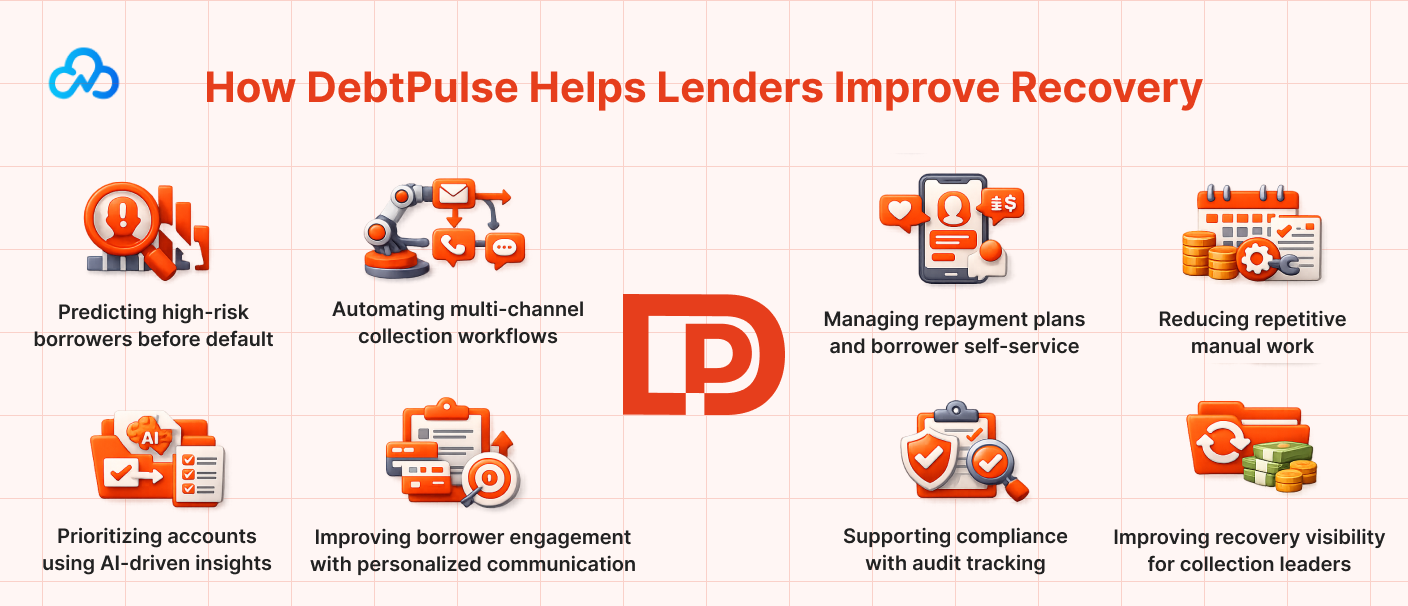

How DebtPulse Helps Lenders Improve Recovery

DebtPulse is an AI-powered debt intelligence and recovery platform built for modern financial institutions.

It helps lenders move from reactive collection work to predictive recovery operations by using AI-driven risk intelligence, borrower segmentation, automation, and portfolio insights.

DebtPulse helps teams with:

- Predicting high-risk borrowers before default

- Automating multi-channel collection workflows

- Prioritizing accounts using AI-driven insights

- Improving borrower engagement with personalized communication

- Managing repayment plans and borrower self-service

- Tracking portfolio performance through real-time dashboards

- Reducing repetitive manual work

- Supporting compliance with audit tracking

- Improving recovery visibility for collection leaders

Instead of depending on spreadsheets, disconnected tools, and manual follow-ups, lenders can use DebtPulse to manage recovery operations with more structure and visibility.

DebtPulse is especially useful for NBFCs, fintech lenders, banks, and loan servicing teams that want to improve recovery rates without increasing manual workload.

Who Should Use Cloud Based Debt Collection Software?

Cloud based debt collection software is useful for:

- NBFCs

- Digital lending platforms

- Banks

- Fintech lenders

- Loan servicing companies

- Embedded finance platforms

- Consumer lending businesses

- Credit providers

- Recovery teams

- Collection agencies working with financial institutions

Any lender managing overdue accounts, EMI reminders, delinquency tracking, repayment follow-ups, or borrower communication should consider using cloud based debt collection software.

Do you like to read more educational content? Read our blogs at Cloudastra Technologies or contact us for business enquiry at Cloudastra Contact Us.

FAQs

1. What is cloud based debt collection software?

Cloud based debt collection software is an online platform that helps lenders manage overdue accounts, automate borrower follow-ups, track repayment behaviour, assign recovery tasks, and monitor collection performance from one system.

2. Why do lenders need cloud based debt collection software?

Lenders need cloud based debt collection software because manual follow-ups become slow and difficult as borrower volume grows. It helps teams automate reminders, prioritize high-risk accounts, track repayments, and maintain audit-ready records.

3. What are the main use cases of cloud based debt collection software?

The main use cases include EMI reminder automation, delinquency tracking, borrower risk scoring, collection workflow automation, promise-to-pay tracking, multi-channel communication, portfolio dashboards, and compliance tracking.

4. Can cloud based debt collection software integrate with CRM systems?

Yes. Many cloud based collection systems can integrate with CRM systems, loan management systems, payment tools, and internal workflows so collection teams can see borrower data, repayment history, and communication records in one place.

5. How does DebtPulse help lenders improve recovery?

DebtPulse helps lenders predict high-risk borrowers early, automate collection workflows, prioritize accounts, personalize borrower communication, track portfolio performance, and maintain compliance records.