The fintech industry has reached a point where regulation is no longer something teams can postpone until later. It now sits at the center of how products are built, launched, scaled and trusted.

That shift matters because the market is still growing fast. The global fintech market was valued at USD 394.88 billion in 2025 and is projected to reach USD 460.76 billion in 2026, with a compound annual growth rate of 18.20% through 2034. But behind that growth is a harder reality: companies that treat fintech regulatory compliance as a side function are more exposed than ever to launch delays, enforcement action, fines and even forced shutdowns.

For founders and CTOs, this changes the operating model completely. Compliance is no longer just a legal requirement. It is product architecture, data governance, workflow design and market readiness. It affects how users are verified, how data is handled, how suspicious activity is reported, how third-party vendors are monitored and how expansion into new markets is planned.

The biggest change in 2025 was not simply that regulators became stricter. It was that they became clearer. The environment moved away from enforcement-heavy skepticism and toward more defined frameworks intended to support innovation while protecting consumers. That sounds like good news and in many ways it is. But it also introduced a more complex reality: more jurisdictions, more specific rules, more scrutiny of technology systems and far less tolerance for weak oversight.

For anyone still asking what is compliance in a fintech context, the answer is broader than policy documentation. It is the practical ability to operate inside regulatory expectations in real time.

Why fintech regulation now shapes business strategy

Over the last eighteen months, fintech regulation has shifted from fragmented oversight to a more strategic and proactive model. Regulators are no longer reacting only after problems appear. They are building frameworks that directly address digital assets, AI, open banking, data rights, sanctions controls and third-party risk.

That has changed how fintech companies are judged.

In the past, some companies operated with an informal assumption that they were “technology platforms” rather than financial institutions. That distinction has weakened. Regulators now increasingly expect fintech companies to meet the same consumer protection standards as traditional financial players, even when the structure is tailored to their business model and risk profile.

That expectation is showing up in real operating pressure. In 2025, many fintech founders said complex paperwork and compliance checks caused more launch delays than competitors. Regulators are no longer satisfied with reviewing static policy files. They want to see how systems function in practice: how user identity is verified, how access is controlled, how monitoring works and how suspicious activity is detected and escalated.

This is one of the clearest signs that financial compliance technology is no longer optional infrastructure. It is part of the core product stack.

A few things now define the new regulatory reality:

- Compliance must be visible in the system, not only in documentation

- Product teams and compliance teams can no longer work in isolation

- Jurisdiction-specific requirements are becoming harder to ignore

- Technology decisions are increasingly treated as compliance decisions

- Third-party partnerships now attract direct regulatory attention

In simple terms, the companies that scale are increasingly the ones that build compliance into the product early.

Capital is flowing toward companies that look regulation-ready

Market behavior is confirming this shift.

Global fintech investment rebounded in 2025, rising to $116 billion across 4,719 deals, up from $95.5 billion across 5,533 deals in 2024. What stands out is not just the amount of capital. It is the drop in deal volume alongside higher total investment. Investors appear to be placing fewer bets and placing them more selectively.

That matters because it suggests something important: capital is moving toward fintech companies with stronger compliance maturity, not simply faster growth stories.

The same pattern shows up in digital assets. Investment in digital asset-focused startups nearly doubled from $11.2 billion in 2024 to $19.1 billion in 2025, helped by the passage of the GENIUS Act in the second half of 2025. Regulatory clarity changed how investors assessed risk and the sector responded quickly.

Geography also plays a role. North America held a 32.30% share of the global fintech market in 2025. The U.S. market is projected to reach USD 99.82 billion by 2026. At the same time, Asia Pacific is expected to grow at the fastest rate, with Japan projected at USD 26.53 billion, China at USD 30.86 billion and India at USD 26.58 billion by 2026.

Exit activity tells the same story. In 2025, global fintech exits reached $104.4 billion across 486 exits, the third-highest year on record. That kind of rebound does not happen in a market that investors think is structurally blocked by regulation. It happens when there is enough confidence that companies can operate, grow and eventually reach liquidity with sustainable regulatory footing.

The compliance areas founders and CTOs can’t afford to treat lightly

1. AML and KYC are still the first line of scrutiny

Anti-money laundering and know your customer obligations remain the foundation of fintech regulation. In 2025, fines issued to financial institutions globally increased by 417% in the first half of the year compared to the same period in 2024, totaling around $1.23 billion. Much of that was driven by enforcement in the digital assets sector.

The reasons behind those penalties are instructive. Common failures included:

- weak transaction monitoring

- gaps in governance and senior oversight

- poor customer due diligence

- failures to identify beneficial owners or sources of funds

- sanctions screening weaknesses

One major enforcement case involved penalties of more than $120 million tied to crypto transaction oversight failures, rapid customer growth outpacing compliance capacity, over-reliance on automated onboarding and failure to stop criminal misuse of accounts.

The message is hard to miss: fast growth without strong compliance controls is now a direct risk factor.

2. Data privacy has become a product-level issue

Data privacy is no longer a legal checkbox. It is part of platform design.

For fintech companies, this means knowing exactly where personal data is collected, stored, processed and transferred. It also means classifying data by sensitivity, applying the right safeguards and reviewing those systems regularly.

Regulators increasingly expect robust governance around data use, especially where AI or automated decisioning is involved. The SEC’s 2026 exam priorities made it clear that firms will be assessed on whether they have adequate policies and procedures to supervise their use of AI technologies.

Enforcement trends also show that companies are being judged on the gap between what they claim and what they actually do. The FTC’s May 2025 settlement with GoDaddy focused on alleged misrepresentation of security protections and required a comprehensive information security program and independent third-party assessment.

For fintech operators, that is a reminder that it compliance includes technical controls, evidence of monitoring and accuracy in how security practices are presented.

3. Open banking and payments rules require precision

Open banking has created new opportunities, but it has also raised the bar on consent, authentication, security and auditability.

PSD2 requires financial institutions to share data with customers in ways that allow approved apps and services to function, while also enforcing strong customer authentication, secure API communication and incident reporting standards. In the U.S., the CFPB outlined data-sharing principles focused on access, scope, consumer control and informed consent.

For fintech teams, this creates a practical challenge: building systems that can handle different requirements across jurisdictions without breaking product consistency.

A single global approach is rarely enough. Companies need flexible architectures that can adapt to local rules around consent, data access, reporting and security.

4. Digital asset rules are becoming more structured, not less

Digital asset regulation changed dramatically in 2025.

In the U.S., the environment shifted from enforcement-heavy skepticism to greater flexibility for market participants engaging with digital assets and distributed ledger technology. The GENIUS Act, signed in July 2025, created the first federal regulatory system for stablecoins, requiring full reserve backing with liquid assets and monthly public reserve disclosures.

It also made stablecoin issuers subject to the Bank Secrecy Act, which clearly connects the market to AML and sanctions obligations.

That clarity had real market consequences. Stablecoins grew to 30% of all on-chain crypto transaction volume and by August 2025 had recorded over USD 4 trillion in annual volume so far, up 83% from the same period in 2024. USDC and USDT together held around 2.25% of the Treasury bill market as of June 30, 2025, equal to US$130 billion.

Outside the U.S., MiCA in the European Union established uniform rules for crypto-assets around transparency, disclosure, authorization and supervision. Other jurisdictions, including Hong Kong, Singapore, Japan, the UK and the UAE, also moved to formalize frameworks.

This is important for any founder working in digital assets: fintech regulations are no longer vague enough to ignore. They are becoming detailed enough to build against.

Recent developments that changed the operating environment

The period from September 2025 through February 2026 brought especially heavy regulatory activity.

The SEC and CFTC announced harmonization efforts and a joint roundtable focused on reducing ambiguity in digital asset oversight. Both agencies signaled openness to innovation exemptions and safer pathways for market participation, including activity involving DeFi protocols and spot crypto assets.

Cybersecurity rules also tightened. The New York Department of Financial Services updated its Cybersecurity Regulation effective November 1, 2025, requiring multi-factor authentication for all user access to all information systems. That is a major signal that regulators increasingly view cybersecurity controls as baseline compliance infrastructure.

At the same time, enforcement against bank-fintech partnerships intensified. Consent orders involving Quaint Oak and Hatch Bank highlighted regulator concern around third-party risk management, AML oversight, independent testing and board-level governance of fintech relationships.

This matters for companies that rely on sponsor banks or regulated partners. Regulators are no longer looking only at the fintech or only at the bank. They are examining the partnership as a shared compliance ecosystem.

AI governance is quickly becoming part of compliance itself

AI moved from a future issue to a current regulatory issue faster than many fintech teams expected.

By 2025, financial institutions were already creating internal AI policies to guide use and meet legal obligations. In 2026, the pressure is increasing as AI becomes more active in customer workflows, decisioning systems and fraud detection.

Regulators are focusing on three things in particular:

- transparency

- fairness

- auditability

Financial institutions using advanced scoring or AI are increasingly expected to keep records of every decision. In Europe, the AI Act classifies credit-scoring models as high-risk systems. Some digital lenders have already had to publish detailed model information before license renewal.

Agentic AI adds another layer of difficulty. As AI-driven workflows take on more actions, attackers may shift toward manipulating inputs, synthetic interactions and false context rather than targeting only user accounts or cards.

That means compliance is no longer only about monitoring financial activity. It is also about governing decision systems.

The hidden question: build on partnerships or seek a charter?

Another major shift in 2025 was the rise in bank charter activity. By October 3, 2025, twenty filings from fintechs and other non-traditional applicants had been submitted in the U.S., an all-time high.

The reasons are understandable:

- some fintechs have reached enough scale to justify the investment

- regulators appear more open to non-traditional applicants

- reliance on sponsor banks creates long-term control risk

At the same time, charter decisions are not simple. National trust bank charters granted to major digital asset firms created momentum, but also triggered criticism that such charters may create regulatory arbitrage because they can avoid certain obligations tied to full-service banks.

For founders and CTOs, the takeaway is not that every fintech should pursue a charter. It is that operating model decisions now have deeper regulatory consequences than before.

Compliance is becoming a major budget line

One of the biggest mistakes early-stage teams make is under-budgeting for compliance.

Compliance costs in fintech increased nearly 30% worldwide between 2023 and 2024. That rise reflects more than legal fees. It includes infrastructure, tooling, specialist hires, advisory support, oversight processes and the operational cost of maintaining readiness across changing rules.

A practical rule emerging from the market is that fintechs not allocating 15% to 20% of their technology budget to compliance infrastructure may be building on unstable foundations.

That sounds heavy, but it fits the reality of the market. A fintech that handles real customers and real money needs clear ownership of compliance. That may not require a full-time executive on day one, but it does require qualified leadership, whether internal or fractional.

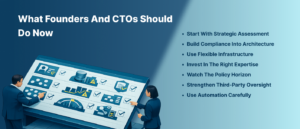

What founders and CTOs should do now

If the regulatory environment feels overwhelming, the response should not be to slow down blindly. It should be to get more structured.

A strong approach now includes:

Start with strategic assessment

Map your business model against licensing requirements, operating markets, data rules and partner dependencies before making irreversible product decisions.

Build compliance into architecture

Treat identity checks, data retention, transaction controls and logging as system design requirements, not add-ons after launch.

Use flexible infrastructure

Per-market configuration for data handling, verification requirements and transaction rules is becoming essential for global expansion.

Invest in the right expertise

A qualified compliance lead, even on a fractional basis, can close major gaps before they turn into product or regulatory problems.

Watch the policy horizon

Regulatory expectations are still evolving. Teams need a process for monitoring changes rather than reacting only when something breaks.

Strengthen third-party oversight

If your business relies on vendors for payments, identity, screening or hosting, your compliance exposure includes theirs.

Use automation carefully

AI-driven monitoring, AML screening and anomaly detection can reduce error and improve scale, but systems must remain explainable and audit-ready.

The global picture is still uneven

The U.S. is moving toward clearer digital asset regulation, but still has federal-state fragmentation. The European Union remains the most prescriptive, with MiCA and broader operational resilience requirements creating a highly structured environment. The UK continues with open banking standards while adapting its own post-Brexit path. In Asia-Pacific, Singapore offers clarity through detailed licensing, while India emphasizes strict KYC, local data handling and regular audits.

So while regulation is becoming clearer, it is not becoming uniform.

That means expansion strategy matters. A company that wants to scale internationally must think not only about product-market fit, but also regulatory-market fit.

Final takeaway: the strongest fintech companies will build with compliance at the center

The clearest lesson from 2025 and early 2026 is that compliance is no longer the layer behind the product. It is part of the product.

Fintech companies that build compliance into architecture, invest in specialist talent, maintain visibility across vendors and partners and engage regulators early are putting themselves in a stronger position to scale with confidence. Those that continue to rely on loose assumptions, patchwork controls or delayed governance are operating on weaker ground.

In the years ahead, the companies most likely to win will not be the ones that avoid regulation. They will be the ones that understand how to build trust, resilience and speed within it. If you are rethinking your approach to fintech regulatory compliance and want to turn these insights into a practical roadmap for your product, team or market strategy, Book a call and start the conversation from a stronger foundation.