Loan recovery automation helps NBFCs and fintech lenders manage overdue borrowers faster by automating reminders, tracking delinquency stages, prioritizing high-risk accounts, and giving collection teams a clear view of recovery actions.

For lenders, the real challenge is not only sending payment reminders. It is knowing which borrower needs attention first, which account is moving toward higher delinquency, which follow-up has already happened, and which case should be escalated before recovery becomes harder. DebtPulse helps lending teams automate these workflows and manage collections with better visibility.

Introduction

NBFCs and digital lenders manage thousands of borrowers across different repayment stages.

Some borrowers miss an EMI by a few days. Some repeatedly delay payments. Some make promises to pay but do not complete them. Some accounts move from early delinquency to serious recovery risk because follow-ups are delayed or poorly tracked.

When collection teams depend on spreadsheets, manual call lists, WhatsApp reminders, and disconnected systems, recovery becomes difficult to control.

Common issues start appearing:

- Borrowers are contacted late

- Agents work on outdated lists

- High-risk accounts are not prioritized

- Promise-to-pay dates are missed

- Managers do not get real-time portfolio visibility

- Early-stage delinquency turns into harder recovery

- Communication history is scattered

- Escalations happen inconsistently

Loan recovery automation solves this by helping lenders organize borrower follow-ups, automate EMI reminders, assign cases, track delinquency movement, and improve collection efficiency from one system.

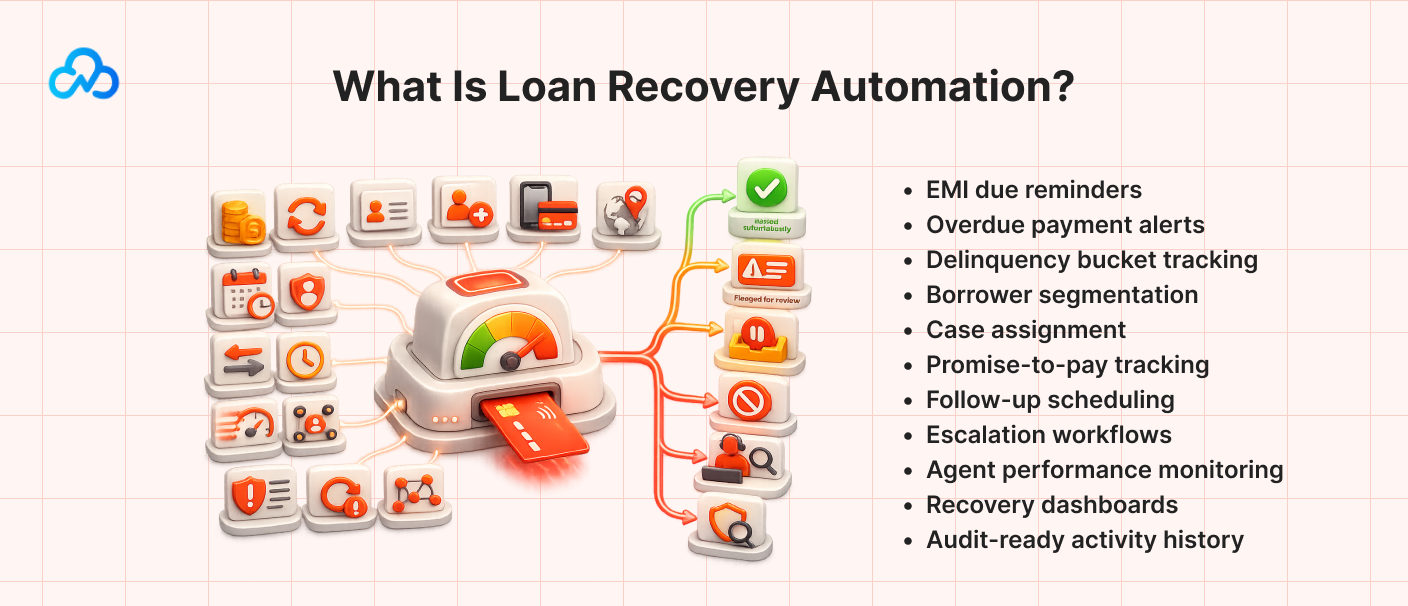

What Is Loan Recovery Automation?

Loan recovery automation is the process of using software to manage overdue loan accounts, automate borrower communication, track repayment status, prioritize risky borrowers, and support collection teams through structured workflows.

It helps lenders manage the full recovery cycle, including:

- EMI due reminders

- Overdue payment alerts

- Delinquency bucket tracking

- Borrower segmentation

- Case assignment

- Promise to pay tracking

- Follow up scheduling

- Escalation workflows

- Agent performance monitoring

- Recovery dashboards

- Audit ready activity history

In simple terms, loan recovery automation helps lenders answer important questions such as:

- Which borrowers are overdue today?

- Which accounts need urgent follow-up?

- Which borrowers promised to pay?

- Which promises were broken?

- Which accounts are moving into higher delinquency?

- Which agent is handling each case?

- Which recovery actions have already happened?

- What is the total overdue exposure by bucket?

Instead of managing recovery manually, lenders get a structured system that keeps every account visible and every action trackable.

Why NBFCs Need Loan Recovery Automation

NBFCs need loan recovery automation because manual recovery workflows cannot keep up with growing borrower volume.

As loan portfolios grow, collection teams have to manage more repayment schedules, more overdue accounts, more borrower conversations, and more follow-up actions.

Without automation, recovery teams often spend too much time on basic operational tasks like preparing lists, checking due dates, sending reminders, updating spreadsheets, and reporting status to managers.

This slows down collection action.

For NBFCs, even a few days of delay can matter. With loan recovery automation for NBFCs, early-stage delinquency can be identified before it moves into deeper buckets, borrowers can be contacted at the right time, missed promise-to-pay follow-ups can be reduced, and high-value overdue accounts can be prioritized instead of getting ignored due to weak manual prioritization.

Loan recovery automation helps NBFCs:

- Act earlier on overdue accounts

- Reduce manual reminder work

- Prioritize borrowers by risk

- Track every recovery action

- Improve agent accountability

- Reduce missed follow-ups

- Improve manager visibility

- Standardize collection workflows

- Support better borrower communication

This is especially important for lenders handling personal loans, business loans, consumer finance, vehicle loans, BNPL, embedded finance, or microfinance portfolios.

How Loan Recovery Automation Works

Loan recovery automation works by connecting loan data, repayment schedules, borrower communication, collection teams, and recovery workflows into one system.

Here is how the workflow usually works.

1. Loan and Repayment Data Sync

The system first connects with the lender’s loan management system, repayment platform, CRM, or internal database.

It pulls important information such as:

- Borrower details

- Loan account number

- EMI amount

- Due date

- Outstanding amount

- Payment status

- Days past due

- Last payment date

- Contact details

- Product type

- Risk category

- Collection stage

This creates one clean view of overdue accounts.

When collection teams work from updated data, they can avoid duplicate follow-ups, missed accounts, and outdated borrower status.

2. Delinquency Bucket Tracking

Once payment data is synced, the system classifies borrowers into delinquency stages.

For example:

- Not yet due

- Due today

- 1–7 days overdue

- 8–30 days overdue

- 31–60 days overdue

- 61–90 days overdue

- 90+ days overdue

This is important because every stage needs a different recovery approach.

A borrower who is 3 days late may only need a soft reminder. A borrower who is 45 days overdue may need stronger follow-up, escalation, or manager review.

Delinquency management helps teams avoid treating every overdue borrower the same way.

3. EMI Reminder Automation

EMI reminder automation helps lenders contact borrowers before and after the due date.

Reminders can be triggered through:

- SMS

- Push notification

- IVR

- In-app message

The system can send reminders based on repayment due date, overdue status, borrower type, previous payment behavior, and risk level.

For example:

- 3 days before due date: soft reminder

- Due date: payment reminder with link

- 2 days overdue: overdue alert

- 7 days overdue: stronger follow-up

- Promise date missed: collection agent alert

This reduces manual work and keeps communication consistent.

4. Borrower Prioritization

Not every overdue borrower should be treated with the same urgency.

Loan recovery automation helps prioritize borrowers based on:

- Days past due

- Overdue amount

- Loan value

- Repayment history

- Broken promises

- Risk score

- Previous communication response

- Borrower segment

- Product type

- Collection stage

This helps collection teams focus on the accounts where action matters most.

For example, a high-value borrower moving from 30 to 60 days overdue may need immediate attention. A low-risk borrower one day late may only need an automated reminder.

Prioritization improves collection efficiency because agents spend more time on accounts that need human action.

5. Case Assignment

Once accounts are prioritized, the system can assign cases to agents or recovery teams.

Each case may include:

- Borrower profile

- Loan details

- Overdue amount

- DPD bucket

- Last reminder sent

- Last contact attempt

- Promise-to-pay status

- Notes

- Risk category

- Next action date

- Escalation status

This gives collection agents full context before they contact the borrower.

Managers can also track which cases are assigned, pending, completed, or overdue for action.

6. Promise-to-Pay Tracking

Promise-to-pay tracking is one of the most important parts of loan recovery.

When a borrower says they will pay on a specific date, that commitment needs to be recorded and tracked.

A good loan recovery software system should track:

- Promise date

- Promise amount

- Borrower response

- Agent note

- Payment status

- Broken promise alerts

- Follow-up action

If the borrower pays, the case can be updated automatically. If the borrower misses the promise date, the system can alert the agent or escalate the case.

This prevents recovery leakage caused by missed manual follow-ups.

7. Escalation Workflow

Some accounts need escalation when borrowers do not respond or delinquency keeps increasing.

Escalation workflows may include:

- Senior agent review

- Manager approval

- Field collection assignment

- Legal notice workflow

- Settlement review

- Restructuring review

- High-risk account tagging

Automation makes escalation more consistent.

Instead of depending on individual judgment or manual reminders, the system can move accounts based on defined rules and recovery policies.

8. Recovery Dashboard and Reporting

Managers need real-time visibility into portfolio health.

A loan recovery automation system should show:

- Total overdue amount

- Bucket-wise delinquency

- Accounts by DPD stage

- Recovery progress

- Agent-wise performance

- Promise-to-pay status

- Broken promises

- Pending follow-ups

- Escalated cases

- Collection efficiency

- Portfolio risk movement

This helps leaders make faster decisions without waiting for manual reports.

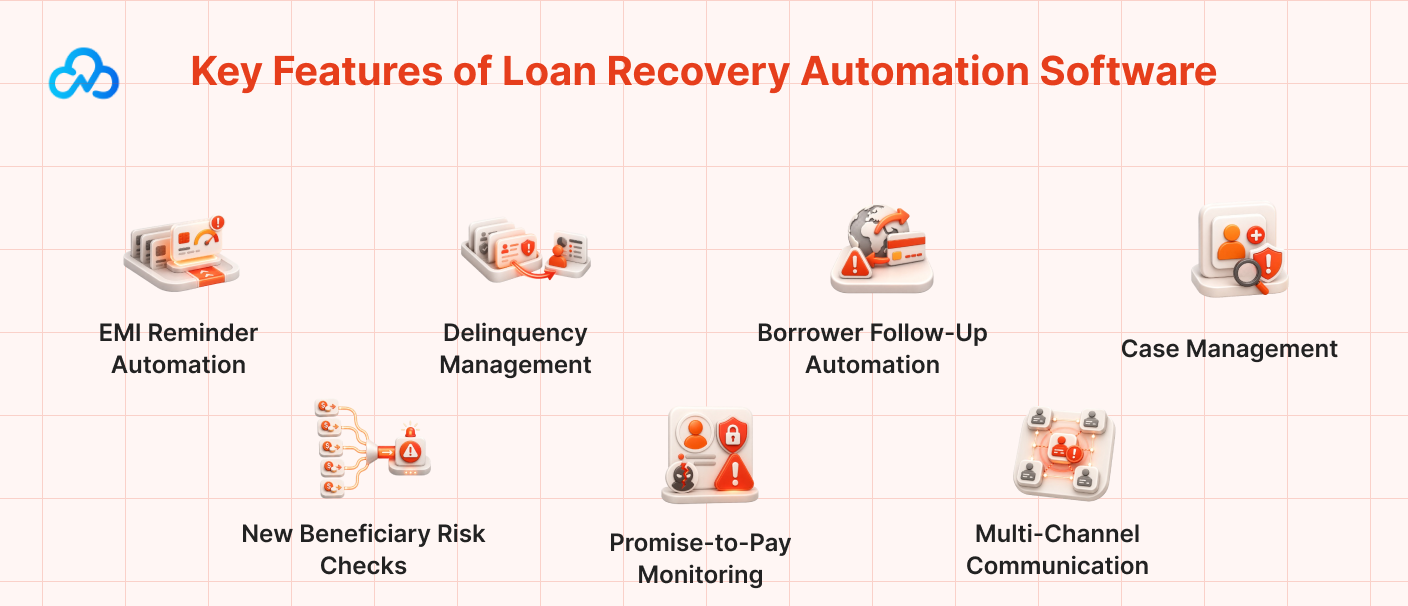

Key Features of Loan Recovery Automation Software

EMI Reminder Automation

Automated reminders help borrowers stay informed about upcoming and overdue EMIs.

This reduces manual follow-up and improves communication consistency.

Delinquency Management

Delinquency management helps lenders track borrowers by overdue stage, amount, risk level, and recovery status.

This makes it easier to take the right action at the right time.

Borrower Follow-Up Automation

Borrower follow-up automation helps teams schedule reminders, assign tasks, track contact attempts, and avoid missed follow-ups.

It ensures every overdue account has a clear next action.

Case Management

Case management helps collection teams manage each borrower account with notes, assignments, repayment status, communication history, and escalation movement.

Promise-to-Pay Monitoring

The system records borrower payment commitments and alerts teams when promises are missed.

This helps improve recovery discipline.

Multi-Channel Communication

Lenders can contact borrowers through SMS, WhatsApp, email, IVR, push notifications, or in-app messages.

Different borrowers respond better to different channels.

Agent Performance Tracking

Managers can track how many cases each agent handles, how many follow-ups are completed, and how much recovery is achieved.

This improves accountability.

Audit Trail

Every reminder, note, assignment, promise, and escalation can be logged.

This helps lenders maintain better internal control and review collection activity when needed.

Use Cases of Loan Recovery Automation

1. Early Delinquency Follow-Up

When borrowers miss an EMI by a few days, automated reminders can help recover payments before accounts move into deeper delinquency.

This is useful for reducing early-stage collection pressure.

2. High-Risk Borrower Prioritization

Collection teams can prioritize borrowers based on risk, overdue amount, repayment history, and days past due.

This helps agents focus on accounts that need human attention first.

3. Promise-to-Pay Recovery

When borrowers commit to paying later, the system tracks the promise and alerts agents if the payment does not happen.

This reduces missed recovery opportunities.

4. Agent Case Assignment

Managers can assign overdue accounts to agents based on location, workload, bucket, product type, or risk level.

This helps teams work in a more organized way.

5. Escalation Management

Cases can be moved to senior review, field action, legal workflow, or settlement review based on predefined conditions.

This improves recovery control.

6. Portfolio-Level Visibility

Lending leaders can see overdue amounts, delinquency movement, recovery progress, and team performance in one dashboard.

This supports faster operational decisions.

Benefits of Loan Recovery Automation

Faster Collection Action

Automation helps teams act earlier instead of waiting for manual lists or delayed reports.

Early action improves the chances of recovery.

Better Borrower Prioritization

Risk-based prioritization helps agents focus on accounts that matter most.

This reduces wasted effort on low-risk or low-priority accounts.

Lower Manual Workload

Teams spend less time on repetitive reminders, spreadsheet updates, and manual tracking.

This allows agents to focus on meaningful borrower conversations.

Improved Recovery Visibility

Managers get a clear view of overdue accounts, bucket movement, agent actions, and portfolio risk.

This improves control over the recovery process.

Consistent Borrower Communication

Automated communication keeps reminders timely and consistent across borrowers.

This reduces confusion and improves borrower experience.

Stronger Collection Accountability

Case assignments, activity logs, and agent dashboards make it easier to track performance.

Managers can see what was done, when it was done, and what needs action next.

Better Escalation Control

Automation helps move cases to the right escalation path when borrowers do not respond or risk increases.

This prevents accounts from being ignored.

Audit-Ready Collection History

Every action is logged, making it easier to review collection activity, borrower communication, and recovery decisions.

Common Mistakes in Loan Recovery Workflows

Waiting Too Long to Contact Borrowers

Delayed follow-up can push accounts into higher delinquency buckets.

Early reminders and quick action are important.

Treating All Borrowers the Same

A first-time late payer and a repeated defaulter should not receive the same recovery workflow.

Segmentation improves recovery strategy.

Depending on Spreadsheets

Spreadsheets create version issues, missed updates, and weak visibility.

They are not reliable for growing loan portfolios.

Not Tracking Promise-to-Pay Properly

If promises are not tracked, follow-ups get missed.

This creates avoidable recovery leakage.

No Clear Escalation Rules

When escalation depends only on manual judgment, cases may move too late or inconsistently.

Defined workflows improve control.

Weak Communication History

Agents need to know what was already communicated to the borrower.

Without history, conversations become repetitive and less effective.

No Real-Time Portfolio Dashboard

Managers need live recovery visibility.

Manual reports are often too slow for fast-moving collection teams.

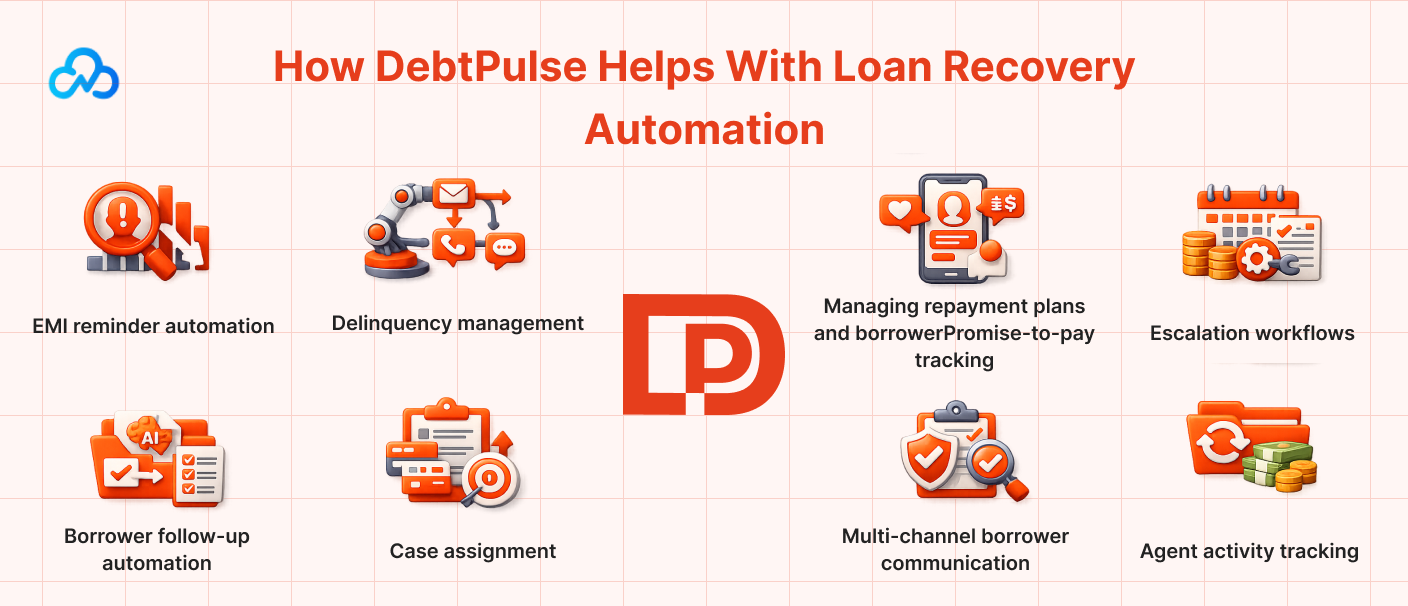

How DebtPulse Helps With Loan Recovery Automation

DebtPulse by Cloudastra helps NBFCs, fintech lenders, banks, and loan servicing teams automate recovery workflows and improve collection visibility.

DebtPulse supports:

- EMI reminder automation

- Delinquency management

- Borrower follow-up automation

- Case assignment

- Promise-to-pay tracking

- Escalation workflows

- Multi-channel borrower communication

- Agent activity tracking

- Portfolio recovery dashboards

- Audit-ready collection history

Instead of managing overdue borrowers through spreadsheets and manual follow-ups, DebtPulse helps teams run a structured recovery process.

It helps lenders know which borrowers need action, which cases are moving into riskier buckets, and which recovery workflows need escalation.

For lending teams that want better control over overdue accounts, DebtPulse brings automation, visibility, and accountability into the recovery process.

Who Should Use DebtPulse?

DebtPulse is useful for:

- NBFCs

- Digital lenders

- Banks

- Fintech lending platforms

- Loan servicing companies

- Embedded finance platforms

- Microfinance institutions

- Credit teams

- Recovery teams

- Collection managers

- Operations leaders

- Risk teams

- Lending product teams

It is especially useful for lenders handling high borrower volume, recurring EMI payments, multiple delinquency buckets, and manual collection workflows.

Want to explore more helpful insights on AI, automation, and enterprise technology? Read more blogs at Cloudastra Technologies or connect with us for business enquiries through Cloudastra Contact Us

FAQs

1. What is loan recovery automation?

Loan recovery automation is the use of software to automate EMI reminders, track overdue borrowers, assign collection cases, monitor delinquency stages, and manage recovery workflows.

2. Why do NBFCs need loan recovery automation?

NBFCs need loan recovery automation because manual follow-ups, spreadsheets, and delayed reporting make it harder to manage growing loan portfolios and overdue borrower accounts.

3. How does loan recovery automation improve collections?

It improves collections by sending timely reminders, prioritizing high-risk borrowers, tracking promise-to-pay commitments, assigning cases, and giving managers real-time recovery visibility.

4. What is delinquency management?

Delinquency management is the process of tracking overdue loan accounts by days past due, repayment status, borrower risk, and recovery stage so lenders can take the right action at the right time.

5. What is EMI reminder automation?

EMI reminder automation sends scheduled repayment reminders to borrowers before and after due dates through channels such as SMS, WhatsApp, email, IVR, push notifications, or in-app messages.

6. How does DebtPulse help collection teams?

DebtPulse helps collection teams automate reminders, track delinquency buckets, assign overdue cases, monitor promise-to-pay status, manage escalations, and view portfolio recovery performance from one system.

7. Can DebtPulse help reduce manual collection work?

Yes. DebtPulse reduces manual work by automating reminders, follow-up scheduling, case tracking, borrower communication history, and recovery reporting.

8. Who should use loan recovery software?

Loan recovery software is useful for NBFCs, fintech lenders, banks, loan servicing companies, embedded finance platforms, and recovery teams that manage overdue borrowers and EMI collections.